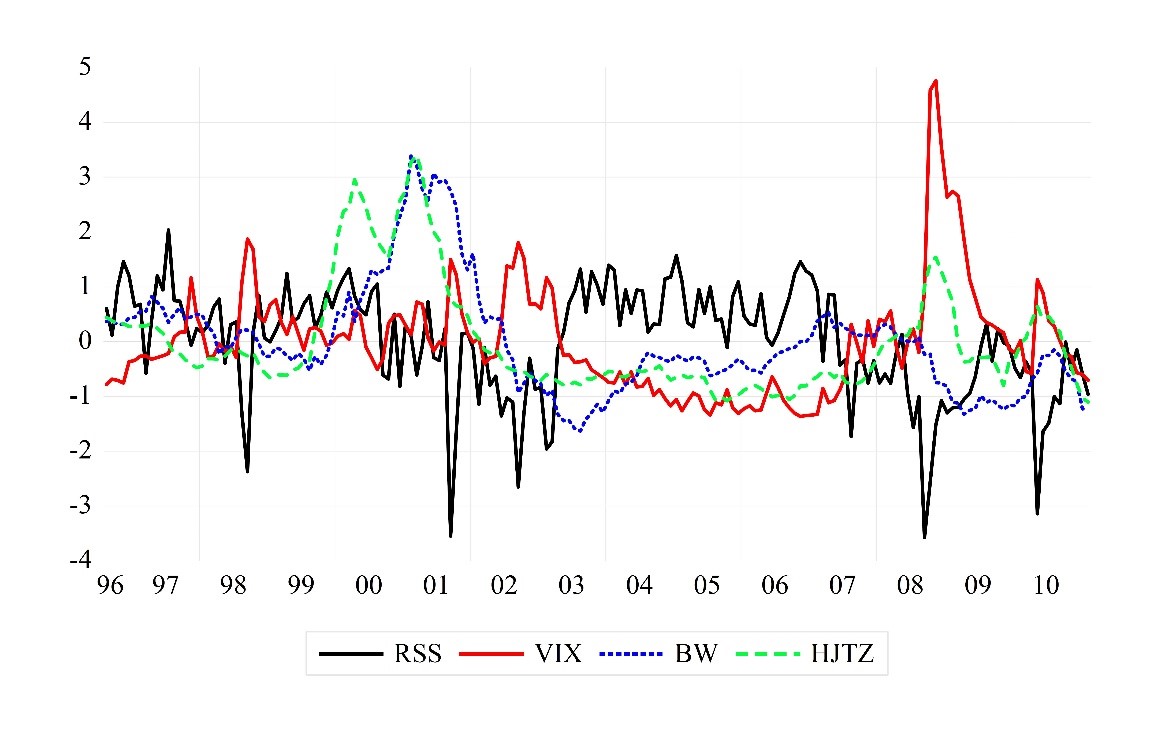

Alternative Measures of Risk

The mainstream measures of risk are derived from the market prices of financial instruments. The study shows that measures constructed by counting the number of words signaling optimism and anxiety in news articles can capture systematic risk. These alternative measures are highly correlated with the traditional measures, but they can provide an additional insight into determinants of financial variables.

Figure. Normalised values of the traditional (VIX) and three alternative risk measures RSS (text based), BW and HJTZ.

Related article:

Demirovic, A., Kabiri, A., Tuckett, D., Nyman, R. (2020). A common risk factor and the correlation between equity and corporate bond returns, Journal of Asset Management, 21(2), pp. 119–134. https://doi.org/10.1057/s41260-020-00151-8.